What is the lowest interest rate on a USDA loan?

What is the interest rate and payback period? Effective October 1, 2022, the current interest rate for Single Family Housing Direct home loans is 3.25% for low-income and very low-income borrowers. Fixed interest rate based on current market rates at loan approval or loan closing, whichever is lower.

Want to learn more about USDA Rural Housing loans? Contact us 7 days a week by calling the number above, or just submit the short Info Request Form on this page. Proud to serve all of Georgia including Valdosta, Thomasville, Tifton, Albany, Columbus, Atlanta, Macon, Savannah, Augusta, Athens, and Marietta.

What is a USDA Ohio Loan? A Ohio USDA Loan is a United States Department of Agriculture sponsored program that is backed by the Government and commonly referred to as Ohio Rural Development loans.

USDA Home Loan Requirements, Credit Score, Approval and Limits in Texas No payments in last 12 months is required. You must be a U.S. citizen or permanent resident. Is your credit score at least 640. Primary residence purchase only. Income limit requirements. This must be in an eligible location.

Is it hard to get approved for a USDA loan?

Qualification is easier than for many other loan types, since the loan doesn't require a down payment or a high credit score. Homebuyers should make sure they are looking at homes within USDA-eligible geographic areas, because the property location is the most important factor for this loan type.

While USDA loans stand out for being ultra-affordable, many borrowers prefer an FHA mortgage for its looser underwriting requirements. There are no income limits when you apply for an FHA loan, and you might be able to get away with a lower credit score and higher debts than USDA or conventional lenders would allow.

What is the income limit for USDA loan in Georgia?

$103,500 Household Income for USDA eligibility â€" In general for 2022, Georgia households with 1-4 members = max $103,500 gross income per year. Some counties can be even higher. Larger households with 5+ members can even go higher, up to $136,600. USDA also allows deductions for child care, elderly, disabilities, etc.

WASHINGTON, Aug. 24, 2022 - The U.S. Department of Agriculture (USDA) announced today up to $550 million in funding to support projects that enable underserved producers to access land, capital, and markets, and train the next, diverse generation of agricultural professionals.

two year USDA encourages lenders to review the previous two year employment history for each applicant, however most income types require a minimum of 12 months on the job to be considered for repayment purposes.

What is the income limit for a USDA loan in Ohio?

To be eligible for a USDA home loan, your total household income cannot exceed the local USDA income limits. The current standard USDA loan income limit for 1-4 member households is $103,500, up from $91,900 in 2021. The 2022 limit for 5-8 member households is $136,600, up from $121,300.

USDA Eligible Areas in Franklin County, Ohio Darbydale. Georgesville. Harrisburg. Pleasant Corners.

How to qualify for an FHA loan in Ohio Minimum credit score of 500. You can qualify for an FHA loan with a credit score of between 500-579, but you'll have to put at least 10% down. Minimum credit score of 580. Debt-to-income ratio (DTI). FHA appraisal costs. Mortgage insurance. Occupancy.

Why would USDA deny a loan?

Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible.

640 To qualify for a USDA loan, you'll need: A minimum FICO ® Score of 640. An eligible property â€" the home you want to buy or refinance must be in an eligible rural or suburban area. Find out if your property is eligible.

Is a USDA loan good? A USDA loan is a great option for buyers with moderate or low income. It lets you buy a house with nothing down and low mortgage rates â€" two huge benefits that only one other loan program (the VA loan) offers. If your home is in an eligible area, it's worth exploring a USDA-guaranteed loan.

How long does it take USDA to approve a loan?

around 30-45 days Once you've signed a purchase agreement, the USDA loan application process typically takes around 30-45 days. The faster all parties work together to complete and provide documents for loan approval, the quicker final loan approval and closing can happen.

41 percent Applicants are considered to have repayment ability when their total debts do not exceed 41 percent of their repayment income. The total debt ratio includes monthly housing expense (PITI) plus other monthly credit or debt obligations incurred by the applicant.

USDA does not underwrite the loans and relies on lenders to make sound underwriting decisions. Lenders must also have a proven ability to originate, underwrite, service, and hold SFH mortgage loans. Therefore, the Agency must approve a lender to ensure that required standards are met and loans will be made responsibly.

What are the two types of USDA loans?

Types of USDA Loans There are only two types of USDA mortgages â€" 15-year fixed-rate loans and 30-year fixed-rate loans. No adjustable-rate mortgages (ARMs) are available to home buyers through the U.S. Department of Agriculture's loan program.

Private mortgage insurance (PMI) is the term used for mortgage insurance on conventional (non-government-backed) loans. So no, USDA loans don't require PMI; only conventional loans have PMI, and only on those loans where the borrower has less than 20% equity in their home.

What does a USDA appraiser look for? Your appraiser will be looking to see that the house and property meet USDA requirements, as well as determining the fair market value based on “comps,†or comparable properties that have recently sold in your area.

What is the highest loan amount for USDA?

The United States Department of Agriculture (USDA) has also increased its maximum loan limit. The 2021 USDA loan limit is $548,250. USDA loans are available to home buyers with low-to-average income for their area.

The primary difference between USDA direct loans and USDA guaranteed loans is who funds the actual loan. With the USDA direct loan, the USDA acts as the lender. Conversely, with the guaranteed loan program, private lenders fund the loan while the USDA backs each loan against default.

USDA annual income is a projection of the total income earned by every adult member of a given household. Remember, each adult occupant's income will be considered when determining USDA income eligibility. That being said, certain types of income are always excluded from this calculation.

What is the USDA guarantee fee for 2022?

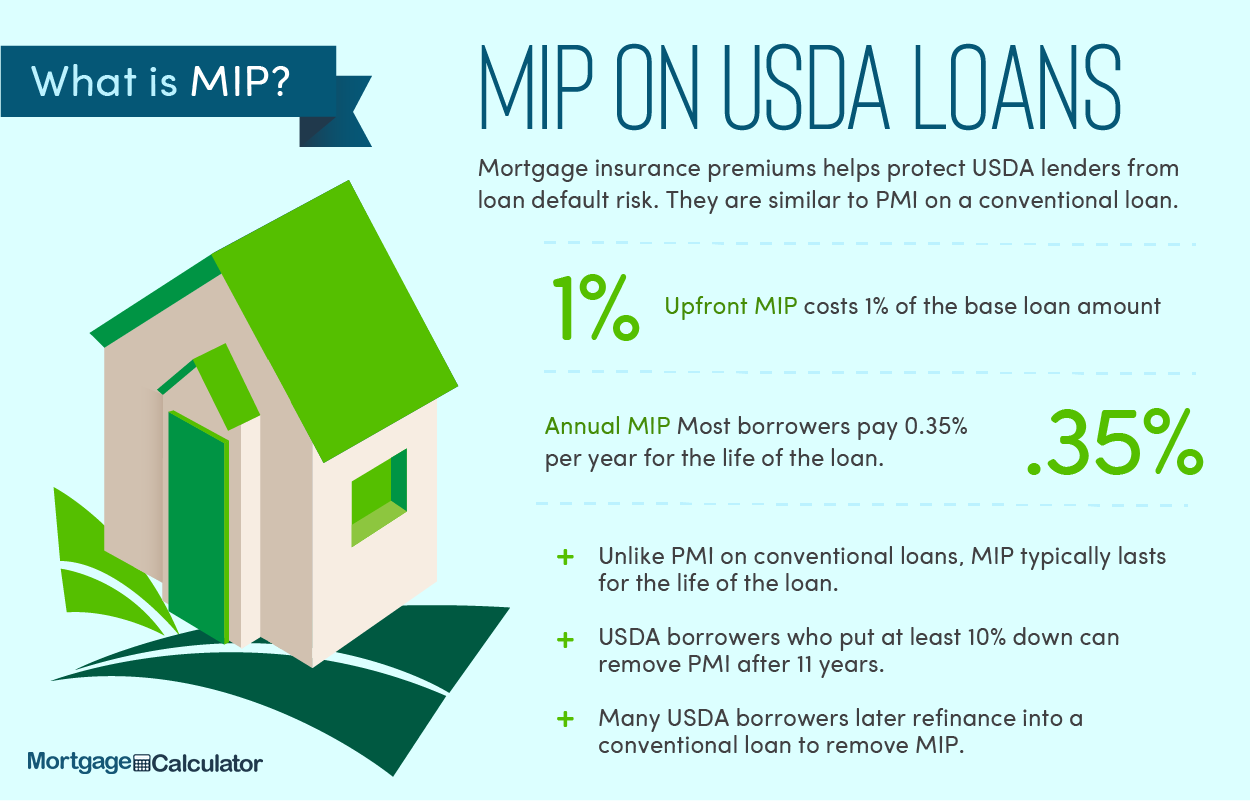

1.0% The USDA Loan fees for FY 2022 are an upfront guarantee fee of 1.0% of the loan amount and an annual fee of 0.35% of the loan amount.

In the 2023 Farm Bill, NSAC will advocate for significant increases in funding for working lands conservation programs, especially for CSP. Increased funding for federal conservation programs is more important than ever.

Under current law, USDA's total outlays for 2021 are estimated at $146 billion. Outlays for mandatory programs are $119 billion, 81 percent of total outlays. Mandatory programs provide services required by law but are not funded through annual appropriations acts.

Do USDA loans get denied?

Beyond these reasons, a USDA loan application could be denied due to inadequate cash savings, spotty employment history, or the house not meeting appraisal guidelines.

640 What is the minimum credit score for a USDA loan? Approved USDA loan lenders typically require a minimum credit score of at least 640 to get a USDA home loan. However, the USDA doesn't have a minimum credit score, so borrowers with scores below 640 may still be eligible for a USDA-backed mortgage.

Asset Documentation: Overview And Bank Statements In order to submit your file to the underwriter, you will need to provide the following USDA Home Loan Asset Documents: Bank statements and 401K or IRA statements.

How long does it take for the underwriter to make a decision?

Underwritingâ€"the process by which mortgage lenders verify your assets, check your credit scores, and review your tax returns before they can approve a home loanâ€"can take as little as two to three days. Typically, though, it takes over a week for a loan officer or lender to complete the process.

Eligibility Requirements â€" Florida Besides a VA loan, this USDA loan is the only 100% no down payment mortgage in Florida. The average household income limits for a USDA home loan in Florida range from $117,900- $155,650 depending on what county you live in.

Shamong Twp. Springfield Twp. Hunterdon County Southampton Twp. Entire county eligible Tabernacle Twp.

What cities qualify for USDA loans in California?

New communities include Atascadero, San Luis Obispo County; Fallbrook, San Diego County; Hollister, St. Benedict County; Paso Robles, St. Louis County; Taft, Kern County; Thermolito, Butte County.

An exclusive right-to-represent agreement is the most popular form of a buyer representation agreement because it gives the licensee the sole right to represent the buyer. Jericho and Cindy, an unmarried couple, have three children, ages 3, 5, and 12.

The Michigan USDA Rural Development loan is a great loan option that allows home buyers to buy a home with no down payment and flexible mortgage terms. You may want to consider a RD Loan if you have had credit issues in the past and do not have money saved for a down payment.

What credit score does FHA require in Ohio?

Credit â€" Most Ohio FHA lenders will require that you have at least a 580 credit score. However, we have a few lenders that will go down to a 500 credit score if you have compensating factors, and if you can place a larger down payment.

Below are our top picks for the best FHA lenders in Ohio: 1.) Quicken Loans. 2.) Guaranteed Rate. 3.) Home Point Financial. 4.) Lynx Financial Group. 5.) Red Brick Mortgage. 6.) Concord Mortgage Group. 7.) Midwest Mortgage Investments. 8.) River City Mortgage.

A major drawback of FHA loans is the high cost of FHA mortgage insurance, which must be paid for the life of the loan if you make the minimum 3.5% down payment. FHA county loan limits also curtail your buying power, since they're set at 35% below conforming conventional loan limits in most counties across the U.S.

What disqualifies a home from USDA financing?

Income-producing properties are ineligible for the USDA home loan. If your property contains a barn, livestock facility, silo, or greenhouse that is no longer in commercial use, there's a chance it may qualify. Discuss the situation with a USDA lender first to be sure.

How long does USDA loan approval take? Depending on your situation, USDA loan approval can take several weeks to over a month â€" generally, 30-60 days. Your loan officer should be able to give you a ballpark time frame.

What can you do? This loan program is NOT just for fixer-uppers and foreclosures! It can be used to upgrade and update any home to meet your specific needs.

Is USDA or FHA better?

While USDA loans stand out for being ultra-affordable, many borrowers prefer an FHA mortgage for its looser underwriting requirements. There are no income limits when you apply for an FHA loan, and you might be able to get away with a lower credit score and higher debts than USDA or conventional lenders would allow.

USDA Loan Requirements Although it is possible to qualify for a USDA loan with collections on your credit report, USDA guidelines state that you must make payment arrangements with the collection agency before it will guarantee your loan.

A total of three credit sources (combination of traditional and alternative) are needed. OR Two sources may be used if one of those sources is a verification of rent or mortgage payments.

Can you pay a USDA loan off early?

The USDA mortgage does NOT have any prepayment or early payoff penalty. You can sell/pay off your loan whenever you like without restriction or fees. This is also the case with other Government-backed loans like FHA and VA.

The applicable upfront guarantee fee and/or annual fee may differ for a purchase and refinance transaction. The annual fee will cease to be collected when 80% loan to value (LTV) is achieved. WAY TO GO! Thank you for supporting the USDA Single Family Housing Guaranteed Loan Program!

Outside of the down payment, one of the biggest appeals of a USDA loan is that it's offered at a low interest rate. In many cases, interest rates for USDA loans are lower than rates for conventional loans. The government backing of USDA loans typically means that lenders can issue them with competitive interest rates.

Is it hard to get approved for USDA?

Qualification is easier than for many other loan types, since the loan doesn't require a down payment or a high credit score. Homebuyers should make sure they are looking at homes within USDA-eligible geographic areas, because the property location is the most important factor for this loan type.

USDA underwriting can take longer than traditional mortgage loans, as it must go through a two-party approval system. Once the lender has underwritten and approved the loan, it must also be approved by the state's USDA office. This can add extra time to the closing process, depending on the state and other factors.

Do USDA loans require tax returns?

USDA requires all applicants to be current on their income tax filings. An applicant with an approved IRS extension for the current tax year may continue to be eligible if they are not delinquent on taxes owed as determined by the IRS.

To be eligible for a USDA home loan, your total household income cannot exceed the local USDA income limits. The current standard USDA loan income limit for 1-4 member households is $103,500, up from $91,900 in 2021. The 2022 limit for 5-8 member households is $136,600, up from $121,300.

How long does USDA take to approve a loan?

around 30-45 days Once you've signed a purchase agreement, the USDA loan application process typically takes around 30-45 days. The faster all parties work together to complete and provide documents for loan approval, the quicker final loan approval and closing can happen.

No, USDA loans do not require private mortgage insurance, or PMI, as PMI only applies to conventional loans. However, USDA loans do have two types of fees that function similarly to PMI. The first is called an upfront guarantee fee, which equals 1 percent of the total loan amount.

Do USDA loans have lower interest rates?

The low interest rate may make it a good time for eligible families to purchase a home through the USDA Rural Development direct loan program. Depending on household incomes, mortgage payments may be further subsidized to as low as one percent interest rate.

Let's review the top five key benefits of USDA rural development loans. No Down Payment Requirements. Most loans require a minimum down payment between 3.5 percent to 20 percent. Flexible Borrower Qualifications. Less Money Spent On Private Mortgage Insurance (PMI) ... Many Properties Can Qualify. Lower Closing Costs.

What is the upfront fee for USDA loans?

1% In order to get a USDA loan, you must pay an upfront guarantee fee. This fee is usually added to the initial loan amount and paid at closing. The new USDA guarantee fee in 2021 costs 1% of the loan amount. This means that if you have a $200,000 home loan, for example, your total loan amount would become $202,000.

What does a USDA appraiser look for? Your appraiser will be looking to see that the house and property meet USDA requirements, as well as determining the fair market value based on “comps,†or comparable properties that have recently sold in your area.

What hurts a home appraisal?

Any unrepaired or ongoing structural damage can hurt your appraisal. Home appraisers are training to look for telltale signs of structural damage, such as cracks in the walls or flooring.

The home's location has the biggest impact on the valuation. The value will be negatively impacted if the home is in an undesirable neighborhood or situated next to a junkyard, power lines, or a busy street.

What is the difference between a USDA loan and a FHA loan?

An FHA loan requires you to make a down payment of 3.5% if your credit score is 580 or higher. For a credit score range of 500 â€" 579, you'll need a 10% down payment. USDA loans, on the other hand, do not require you to come up with a down payment at all. That's one of the most appealing factors of a USDA loan.

41% To get a USDA loan, you must have a DTI of less than 41%. USDA loans have a couple of unique requirements. First, you can't get a USDA loan if your household income exceeds 115% of the median income for your area.

FHA Debt-to-Income Ratio Requirement With the FHA, you're generally required to have a DTI of 43% or less, though it varies based on credit score. To be more specific, your front-end DTI (monthly mortgage payments only) should be 31% or less, and your back-end DTI (all monthly debt payments) should be 43% or less.

What is the maximum square footage for a USDA loan?

For USDA direct loans, properties need to be 2,000 square feet or less and cannot have an in-ground swimming pool. Occupancy: You can only use single family USDA loans for a primary residence, not a second home.

Types of USDA Loans There are only two types of USDA mortgages â€" 15-year fixed-rate loans and 30-year fixed-rate loans. No adjustable-rate mortgages (ARMs) are available to home buyers through the U.S. Department of Agriculture's loan program.

Also known as the Section 502 Direct Loan Program, this program assists low- and very-low-income applicants obtain decent, safe and sanitary housing in eligible rural areas by providing payment assistance to increase an applicant's repayment ability.

Does USDA require bank statements?

Asset Documentation: Overview And Bank Statements In order to submit your file to the underwriter, you will need to provide the following USDA Home Loan Asset Documents: Bank statements and 401K or IRA statements.

While standard USDA loan qualifying ratios (otherwise known as debt ratios) assume that income is taxable, USDA guidelines calculate tax exempt income differently. When certain sources of income are not subject to federal tax, they can then be grossed up by 25%. Examples of this income are: Social Security Income.

Required Documentation: Federal income tax returns or IRS transcripts with all schedules Evidence of additional property or assets retained by the applicant through title, bank statements, etc.

What is the downside to a USDA loan?

The main downside that stops people from taking out USDA loans is the geographic restrictions. As USDA loans are only designed for rural areas mostly, it means that anyone who wants to buy a home in a more urban location cannot qualify.

640 What is the minimum credit score for a USDA loan? Approved USDA loan lenders typically require a minimum credit score of at least 640 to get a USDA home loan. However, the USDA doesn't have a minimum credit score, so borrowers with scores below 640 may still be eligible for a USDA-backed mortgage.

If you make a down payment of less than 10%, you'll pay mortgage insurance for the life of the loan. If you make a down payment of 10% or more, you'll pay it for 11 years.

What is it called when the government pays farmers not to farm?

The Agricultural Adjustment Act (AAA) was a United States federal law of the New Deal era designed to boost agricultural prices by reducing surpluses. The government bought livestock for slaughter and paid farmers subsidies not to plant on part of their land.

These laws are -- The Farmers' Produce Trade and Commerce (Promotion and Facilitation) Act, The Farmers (Empowerment and Protection) Agreement of Price Assurance and Farm Services Act, and The Essential Commodities (Amendment) Act.

One bill relaxes restrictions governing purchase and sale of farm produce, the second relaxes restrictions on stocking under the Essential Commodities Act (ECA), 1955, and the third introduces a dedicated legislation to enable contract farming based on written agreements.

Has USDA been funded for 2022?

WASHINGTON, Aug. 24, 2022 - The U.S. Department of Agriculture (USDA) announced today up to $550 million in funding to support projects that enable underserved producers to access land, capital, and markets, and train the next, diverse generation of agricultural professionals.

1.0% The USDA Loan fees for FY 2022 are an upfront guarantee fee of 1.0% of the loan amount and an annual fee of 0.35% of the loan amount.

In the 2023 Farm Bill, NSAC will advocate for significant increases in funding for working lands conservation programs, especially for CSP. Increased funding for federal conservation programs is more important than ever.

What disqualifies a home from USDA financing?

Income-producing properties are ineligible for the USDA home loan. If your property contains a barn, livestock facility, silo, or greenhouse that is no longer in commercial use, there's a chance it may qualify. Discuss the situation with a USDA lender first to be sure.

640 To qualify for a USDA loan, you'll need: A minimum FICO ® Score of 640. An eligible property â€" the home you want to buy or refinance must be in an eligible rural or suburban area. Find out if your property is eligible.

Even though USDA Direct Loans are underwritten by the USDA, home buyers can still expect a 30-60 day timeline for loan approval.

Is USDA or FHA better?

While USDA loans stand out for being ultra-affordable, many borrowers prefer an FHA mortgage for its looser underwriting requirements. There are no income limits when you apply for an FHA loan, and you might be able to get away with a lower credit score and higher debts than USDA or conventional lenders would allow.

USDA Loan Requirements Although it is possible to qualify for a USDA loan with collections on your credit report, USDA guidelines state that you must make payment arrangements with the collection agency before it will guarantee your loan.

Is it possible to raise a credit score quickly? No. 1: Check your credit report for errors. No. 2: Consider Experian Boost. No. 1: Pay your bills on time. No. 2: Practice responsible credit card use. No. 3: Consider asking a trusted source for help. No. 4: Pay down your debts as aggressively as possible.

Does USDA allow future income?

If the applicant has a minimum of 1 year of continuous stable and dependable income, future/projected income may still be considered when the applicant has a firm offer with the employer without a foreseeable or unjustifiable gap in employment.

Yes, a mortgage lender will look at any depository accounts on your bank statements â€" including checking accounts, savings accounts, and any open lines of credit. Why would an underwriter deny a loan? There are plenty of reasons underwriters might deny a home purchase loan.

Applicants may have only one guaranteed or direct loan at one time. Judy must close on the sale of her current guaranteed home before she can complete the purchase of the new home. USDA must ensure that there is a bedroom for each household dependent in order for the home to be considered adequate for the household.

What are red flags for underwriters?

General Red Flags verifications that are completed on the same day as ordered or on a weekend/holiday. homeowner's insurance is a rental policy. different mailing addresses on bank statements, pay stubs and W-2s. assets are not consistent with the income.

Tip #1: Don't Apply For Any New Credit Lines During Underwriting. Any major financial changes and spending can cause problems during the underwriting process. New lines of credit or loans could interrupt this process. Also, avoid making any purchases that could decrease your assets.

How often do underwriters deny loans? Underwriters deny loans about 9% of the time. The most common reason for denial is that the borrower has too much debt, but even an incomplete loan package can lead to denial.

How do I qualify for a USDA loan in Florida?

USDA eligibility requirements Minimum credit score: 640 with most lenders. Clean credit history: No late payments or recent bankruptcy or foreclosure. Income requirements: household income limits vary by area; often $91,900 for a 1-4 person household. Employment: Borrowers need a steady income and employment history.

Florida USDA Mortgage Approved Locations Include: Locations outside of Orlando like Ocoee, Winter Garden, Kissimmee, and Osceola County, may still be eligible. Locations outside of Tampa like Riverview, Valrico, Ruskin, Sun City, Wesley Chapel Pasco, Odessa, Pasco County still have approved areas.

The adjusted annual income calculation will determine if the household is eligible for the guaranteed loan program. Adjusted annual income is calculated by using the annual income figure and subtracting any of the eligible deductions in 3555.152(c) for which the household may qualify.

Does USDA mortgage insurance?

United States Department of Agriculture (USDA) direct loans have no mortgage insurance. USDA guaranteed loans are charged an annual guarantee fee instead of mortgage insurance. Guarantee fees are paid to USDA by the approved lender and are usually included in the homeowner's monthly loan payment.

502 Direct Housing Loans and. 504 Repair Grant/Loan Program. Direct 502 - Subsidized Mortgages Available to Low. and Very Low Income Families. PURPOSE: To provide affordable housing to low and very low income.

USDA Rural Development's Section 502 Direct Loan Program provides a path to homeownership for low- and very-low-income families living in rural areas, and families who truly have no other way to make affordable homeownership a reality.

How long is a USDA pre approval good for?

for 90 days With most lenders/banks a new loan pre approval letter is valid for 90 days from the date of the initial mortgage application.

Rural areas can still be found in Southern California, in places like East County San Diego and maybe Riverside County, but the cost of real estate is high in many parts of the state and generally unaffordable. California counties considered mostly rural: Amador. Calaveras. Inyo. Lassen. Modoc. Mono. Plumas. Siskiyou.

Shamong Twp. Springfield Twp. Hunterdon County Southampton Twp. Entire county eligible Tabernacle Twp.

Which listing agreement is the most commonly used?

exclusive right-to-sell listing An exclusive right-to-sell listing is the most commonly used contract. With this type of listing agreement, one broker is appointed the sole seller's agent and has exclusive authorization to represent the property.

When considering loan risk, which two items will lenders consider in equal measure? The property's value (as underlying collateral) and the borrower's ability to repay the loan will be equal considerations for the lender.

The answer is - the age of the seller. Information needed for the listing agreement includes lot size, possibility of seller financing, and the property taxes. The age of the seller is not needed.

How do I qualify for a USDA loan in Michigan?

Eligibility Requirements â€" Michigan For a family of 1-4 in Michigan, the average household income limit for a USDA loan is about $129,400, and for a family of 5 or more it can be as high as $170,800. Want to learn more? Fill out the form above to get in touch with one of our USDA loan specialists.

The Michigan State Housing Development Authority (MSHDA) offers Down Payment Assistance (DPA) to specifically help repeat homebuyers purchase a home. The assistance is provided with a zero-interest, non-amortizing loan with no monthly payments.

What banks do FHA loans in Ohio?

Below are our top picks for the best FHA lenders in Ohio: 1.) Quicken Loans. 2.) Guaranteed Rate. 3.) Home Point Financial. 4.) Lynx Financial Group. 5.) Red Brick Mortgage. 6.) Concord Mortgage Group. 7.) Midwest Mortgage Investments. 8.) River City Mortgage.

You can qualify for an FHA loan with a credit score of between 500-579, but you'll have to put at least 10% down. Minimum credit score of 580. A lot of people are attracted to FHA loans because of the low 3.5% down payment requirement. But your credit score must be at least 580 to qualify for this lower requirement.

What credit score does FHA require in Ohio?

Credit â€" Most Ohio FHA lenders will require that you have at least a 580 credit score. However, we have a few lenders that will go down to a 500 credit score if you have compensating factors, and if you can place a larger down payment.

You meet credit score requirements: Conventional, USDA and VA Loans: 640 or higher. FHA Loans: 650 or higher.

Why do sellers not like FHA?

The other major reason sellers don't like FHA loans is that the guidelines require appraisers to look for certain defects that could pose habitability concerns or health, safety, or security risks. If any defects are found, the seller must repair them prior to the sale.

30 to 45 days The typical timeline from application to closing with an FHA loan ranges from 30 to 45 days. During this time, your loan file goes through underwriting. The underwriter takes a closer look at your application and reviews supporting documents to ensure you meet the minimum guidelines for FHA financing.

FHA loans are backed by the Federal Housing Administration and offered by FHA-approved lenders. FHA loans allow smaller down payments (as low as 3.5%) and lower credit scores than most conventional loans. Unlike FHA loans, conventional loans are not insured or guaranteed by the government.

What is the downside to a USDA loan?

The main downside that stops people from taking out USDA loans is the geographic restrictions. As USDA loans are only designed for rural areas mostly, it means that anyone who wants to buy a home in a more urban location cannot qualify.

Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible.

Types of USDA Loans There are only two types of USDA mortgages â€" 15-year fixed-rate loans and 30-year fixed-rate loans. No adjustable-rate mortgages (ARMs) are available to home buyers through the U.S. Department of Agriculture's loan program.

What disqualifies a home from USDA financing?

Income-producing properties are ineligible for the USDA home loan. If your property contains a barn, livestock facility, silo, or greenhouse that is no longer in commercial use, there's a chance it may qualify. Discuss the situation with a USDA lender first to be sure.

The underwriting analysis is a detailed evaluation of key elements of borrower experience and creditworthiness, market conditions, the value of improvements, and the ability of the property to attract the rents needed to generate sufficient cash flow to support the loan's debt service.

The low interest rate may make it a good time for eligible families to purchase a home through the USDA Rural Development direct loan program. Depending on household incomes, mortgage payments may be further subsidized to as low as one percent interest rate.

What does an appraiser look for in a USDA loan?

What does a USDA appraiser look for? Your appraiser will be looking to see that the house and property meet USDA requirements, as well as determining the fair market value based on “comps,†or comparable properties that have recently sold in your area.

Even if you don't have a 640 credit score, it's still possible to apply and be approved for a USDA loan. USDA allows lenders to underwrite and approve USDA home loans manually at the lender's discretion. Once cleared by your lender, the USDA must review your loan for final loan approval before you can close.

If you're considering house hacking, the best deals are VA and USDA loans if you qualify for them. These loans have high upfront fees, but they require a 0% down payment. Borrowers may also want to consider a 5% down payment conventional mortgage.

Are USDA interest rates lower than FHA?

The lack of a down payment requirement makes a USDA loan a more affordable option upfront. Additionally, because they carry lower mortgage insurance rates, USDA loans are often an overall more affordable option than FHA loans for buyers who qualify.

The process of getting a USDA loan may take longer than an FHA loan, largely because USDA loans are underwritten twice, first by the lender and then by the USDA. To have the loan automatically underwritten by the USDA, you'll need a credit score of 640 or higher.

The main benefit to you is that you can get low mortgage interest rates, even without a down payment. Be aware, however, that if you put little or no money down you will have to pay a mortgage insurance premium. The loan term is a 30-year fixed-rate mortgage.

Which FICO score does USDA use?

640 To qualify for a USDA loan, you'll need: A minimum FICO ® Score of 640. An eligible property â€" the home you want to buy or refinance must be in an eligible rural or suburban area. Find out if your property is eligible.

41 percent Applicants are considered to have repayment ability when their total debts do not exceed 41 percent of their repayment income. The total debt ratio includes monthly housing expense (PITI) plus other monthly credit or debt obligations incurred by the applicant.

If you're planning to apply for a USDA mortgage, you may wonder “How much can you borrow with a USDA loan?†With USDA Guaranteed loans, there's no limit on the total amount of money you can borrow to cover the cost of your property's current market value.

Is USDA or FHA better?

While USDA loans stand out for being ultra-affordable, many borrowers prefer an FHA mortgage for its looser underwriting requirements. There are no income limits when you apply for an FHA loan, and you might be able to get away with a lower credit score and higher debts than USDA or conventional lenders would allow.

Lenders must continue to review the applicant credit history in full to determine if they have a history of an ability and willingness to pay their debts. Reminder: USDA does not require medical collections to be paid.

Most mortgage lenders accept FICO scores of 580 and above for an FHA loan. And you only need 3.5% down to buy a house with this program. Some lenders even allow credit scores of 500-579 under the FHA program, though you'll need a 10% down payment if your score is in that range.

What is the highest loan amount for USDA?

The United States Department of Agriculture (USDA) has also increased its maximum loan limit. The 2021 USDA loan limit is $548,250. USDA loans are available to home buyers with low-to-average income for their area.

The USDA Single Family Direct Loan program requires escrow accounts for real estate taxes and hazard insurance. Once an escrow account is established, the Rural Housing Service is responsible for timely payment of taxes and insurance for the duration of the loan.

Private mortgage insurance (PMI) is the term used for mortgage insurance on conventional (non-government-backed) loans. So no, USDA loans don't require PMI; only conventional loans have PMI, and only on those loans where the borrower has less than 20% equity in their home.

What is the USDA monthly fee?

The annual fee is usually financed into your loan. The annual fee currently costs 0.35% of the loan amount for 2021. You will pay this fee monthly along with your monthly mortgage payment throughout the life of your loan.

No, USDA loans do not require private mortgage insurance, or PMI, as PMI only applies to conventional loans. However, USDA loans do have two types of fees that function similarly to PMI. The first is called an upfront guarantee fee, which equals 1 percent of the total loan amount.

An upfront guarantee fee of 1.00 percent and an annual fee of . 35 percent will apply to both purchase and refinance transactions for FY 2022.

Tidak ada komentar untuk "What is the lowest interest rate on a USDA loan?"

Posting Komentar